There are over 300 million people around the world living in fragile contexts, with nearly 26 million refugees fleeing conflict and scarcity. With historically high numbers of people living in crisis – for increasingly protracted periods of time – CARE is committed to supporting people’s economic security, ability to navigate crises, and ultimately recover.

The combination of CARE’s successful Village Savings and Loans Association (VSLA) model and Cash and Voucher Assistance (CVA) can support improved outcomes for crisis-affected populations, and more efficient and effective humanitarian interventions. CVA can help individuals and households meet emergency needs; while VSLA’s are a safety net that can enhance an individual’s capacity to save and borrow, and subsequently rebuild their lives. Since women and girls face disproportionate burdens from crisis, both allow for women to be active in responding to emergencies and bring practical and effective solutions to light. Together, VSLAs and CVA can be powerful tools to address the unique constraints faced by people in crisis.

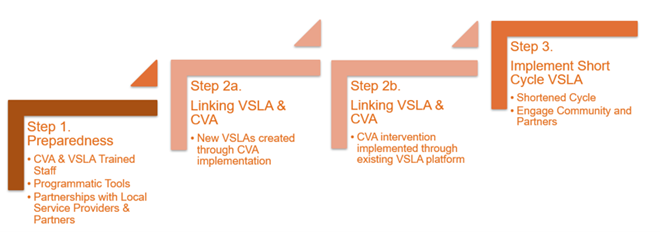

Over the last 18 months, CARE consulted over 125 specialists across 45 countries - from CARE country offices, and other humanitarian and development agencies – to understand when, where and how VSLAs can support emergency response. Key insights have contributed to the development of CARE’s new VSLA in Emergencies (VSLAiE) model, designed to support the effective combination of VSLAs and CVA in humanitarian programs. The VSLAiE model is comprised of three main stages:

In humanitarian contexts, contingency planning and preparedness are critical steps that enable organizations to respond quickly and effectively during a crisis. This stage places an emphasis on being prepared with staff experienced in both VSLA and CVA implementation and gearing that staff with ready-made, “off-the-shelf” tools such as master agreements, standard operating procedures (SOPs), market research, and needs and gender assessment tools. Additionally, it is critical to establish partnerships with trusted local actors (community-based organizations, local and national governments, and financial and non-financial service providers) serving targeted communities.

If cash transfers are not sequenced and timed correctly with VSLAs, and communicated clearly to target communities, benefits may not be properly understood, thus creating adverse effects. This phase includes an assessment of the market, gender norms, and other needs as well as deliberate identification and targeting of households. Conversations with the community about cash and the importance of saving through VSLAs to support recovery assists in sensitizing leaders, partners, and potential participants to the benefits of both VSLAs and CVA. To minimize potential conflict, communities should be involved in the development of selection criteria and the identification of beneficiary households.

The traditional 12-month VSLA cycle can be shortened in complex settings to meet the needs of displaced populations who are often mobile and in transition. It is key to engage the community and partners through feedback and accountability mechanisms (FAM) to address potential risks, conflict, and gender-based violence.

Steps to integrate VSLAs into humanitarian programming

Steps to integrate VSLAs into humanitarian programming

As Technical Advisor, VSLAs in Emergencies, Natacha Brice leads CARE’s work to integrate VSLAs into humanitarian programming. Over the next year, in partnership with the Sall Foundation, CARE will implement a series of pilot projects in Ethiopia, Nigeria and Yemen to test and further refine its VSLAiE model. For more information about CARE’s VSLAiE program, and to share your experience in promoting Savings Groups in emergency contexts, please contact Natacha at natacha.brice@care.org.

Categories: Financial Inclusion Savings Groups English Savings Groups Blog Blog 2021 WebinarsBlogs

![]()

1621 North Kent Street, Ste 900,

Arlington, VA, 22209

P 202.534.1400

F 703.276.1433

Website Photos: © mari matsuri