This case study from Amhara, a region in Ethiopia, highlights lessons learned from access to finance interventions within the Land Investment for Transformation Programme (LIFT). We look at how the programme has enabled the successful design of a new individual loan product by the Amhara Credit and Savings Institution (ACSI).

Land tenure insecurity is a widespread problem in developing countries, where the majority of households are smallholders and depend on subsistence agriculture: uncertainty around tenure leads to farmers not investing in their land, which in turn means low productivity and vulnerability to shocks. Donors such as DFID, USAID and the WB, along with partner country Governments, are investing in increasing the farmers’ security of land tenure through land registration initiatives.

This is why the UK Aid-funded LIFT project works with the Government of Ethiopia (GoE) to deliver Second Level Land Certificates (SLLC) to smallholder farmers and to create a national database to manage and update SLLC data and land related transactions, the Rural Land Administration System (RLAS). The introduction of SLLC and the RLAS is expected to improve both the administration and management of land in Ethiopia. Indeed, a better functioning land system and an increased security of tenure create opportunities for improving the livelihoods of rural dwellers. LIFT works to leverage these opportunities by applying market systems thinking to access to finance interventions.

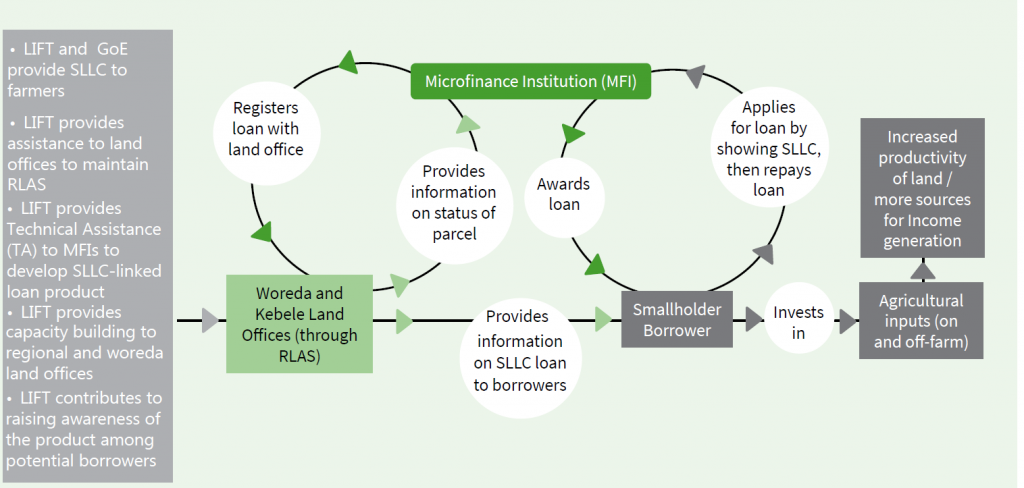

Ethiopian smallholder farmers are underbanked: microfinance institutions (MFIs) currently serve around 20% of estimated market demand. Without means of accessing credit to invest in productive activities, farmers struggle to escape poverty: they need to sell their assets to cover cyclical expenses. LIFT has worked with GoE stakeholders and partner MFIs to develop a loan product for farmers with SLLCs, to allow them to access larger loans on an individual basis. The land tenure regime in Ethiopia specifies that land is owned by the State. To address this difficulty LIFT and its partner MFIs introduced an innovation: the produce of the land can be used as a guarantee to secure a loan.

Figure 1: How the SLLC product works

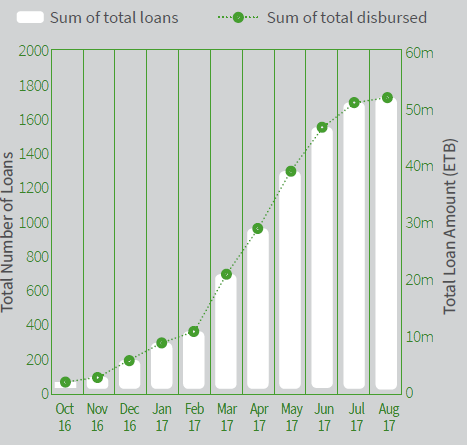

The SLLC product presented in Figure 1 is currently being piloted in three regions through six MFI partners. As of September 2017, over 3,000 SLLC linked loans totalling Birr 83M (USD 3.54M) have been disbursed, with very positive feedback from clients and MFIs (as shown in Figure 2).

Figure 2: SLLC-loan disbursement figures

In this case study, we detail the experiences of MFI partner Amhara Credit and Savings Institution (ACSI), highlighting two key factors behind their successful pilot: stakeholder buy-in and an understanding of customer demand.

Throughout the design phase, ACSI and LIFT adopted a bottom-up approach: ACSI branches developed the SLLC-linked loan product manual in collaboration with the head office staff and the LIFT team, increasing awareness and branch ownership of the product from the start. ACSI management receive weekly updates from branches regarding product progress. They noticed some branch managers were reluctant to give out SLLC-linked loans. When prompted, it emerged branch managers found the new loan ceiling of 50,000 ETB intimidating, since they were used to a maximum loan amount of ETB 15,000 per client. Senior managers are now exploring ways to address the issue.

An important factor supporting the SLLC-linked loan pilot has been the joint engagement by LIFT and MFI partners to better understand the MFI client-base. Joint monitoring visits are regularly organized to assess farmer response to and demand for the product and how it impacts on their lives. Findings are systematically relayed to the MFI Head Office, who in turn share regular information on the product’s performance with the LIFT team. From the farmers’ perspective, there are indications that demand for the loan product is rising. A Woreda Land Administration Official mentioned that, in kebeles where SLLC certification is still on-going, farmers are already opening savings accounts at ACSI so they are eligible to access the loan as soon as they get their certificate.

What are farmers using the loans for? ACSI assesses applicants’ merits to access the loan on the basis of a solid business plan with a strong emphasis on commercially viable agricultural activities. These include:

ACSI expects 99%-100% repayment rates on the loan given how it is performing to date.

Individual SLLC-linked loans were piloted by ACSI in a select number of branches and woredas from September 2016. The idea was to test the approach with a limited group of beneficiaries, and based on the results decide whether the product was viable. If needed, the product could then be refined ahead of roll-out. In June 2017, the LIFT team conducted an assessment of the pilot as part of a routine visit to ACSI. Several interesting indications of behavioural change were identified:

The initial results of the product pilot have been positive, with strong indications of partner ownership and increasing demand for the product from farmers. Following the success of the pilot phase, LIFT will assist ACSI with scale-up. Immediate activities will focus on working with ACSI to better define and understand the target market for the product; help them to price the product appropriately; and improve their capacity to manage and administer an individual lending product.

Clara Garcia Parra is involved in the development and implementation of monitoring, evaluation and learning (MEL) frameworks in private sector development projects. She brings a strong understanding of data and change management, and has conducted and overseen the setup of results measurement systems across short and long-term assignments. Through these, Clara has been successful in supporting implementation teams in jointly developing MEL and knowledge management systems. Her experience ranges from working in projects involving the disbursement of funds, such as DANIDA-funded UNNATI project in Nepal, to working in projects that adopt market systems thinking, such as the DFID-funded Ethiopia Land Investment for Transformation (LIFT) and the Ghana Market Development Programme (MADE).

Categories: Financial Inclusion Sub-Saharan Africa Financial Security Rural and Agricultural Finance Agriculture & Food Security English Unpublished Resources Blog Published Blogs/Webinars Agriculture & Food Security Blog Resources WebinarsBlogs

![]()

1621 North Kent Street, Ste 900,

Arlington, VA, 22209

P 202.534.1400

F 703.276.1433

Website Photos: © mari matsuri